Congratulation to the Employee of the Federal Govt. Finally the notification came for the increase in the BPS of Govt Employee. The notification issued by the Finance Division Of Islamic Republic Of Pakistan. You can download the copy of notification of Revised BPS from the link given below.

Revision of Basic Pay Scales & Allowances of Civil Servants of the Federal Government (2022)

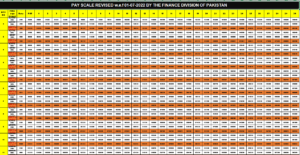

Here is the new revised BPS chart for the GOVT employee to check and fix there pay by the help of the given chart after including the five ad-hoc allowances. The increase in the salary will be on the BPS of 2017 first and then the Ad-hoc allowances will be merged into the basic pay. After that new stages will be created according to the chart. The employee may be get increased in pay by new stage. The difference will be add into the pay.

Download the new salary chart in form of excel sheet and fix your pay.

WAPDA Employee’s Documents

WAPDA Employee’s Documents